How the 10-Year Rule Can Erase Back Taxes Legally: IRS Debt Forgiven After 10 Years

IRS Debt Forgiven After 10 Years

Many taxpayers wonder if they can have their IRS debt forgiven after 10 years. The answer is yes, under specific conditions. The IRS has a statute of limitations on how long it can collect back taxes, known as the Collection Statute Expiration Date (CSED). If your debt reaches that point without resolution, the IRS may no longer legally pursue collection.

What Is the IRS 10-Year Rule?

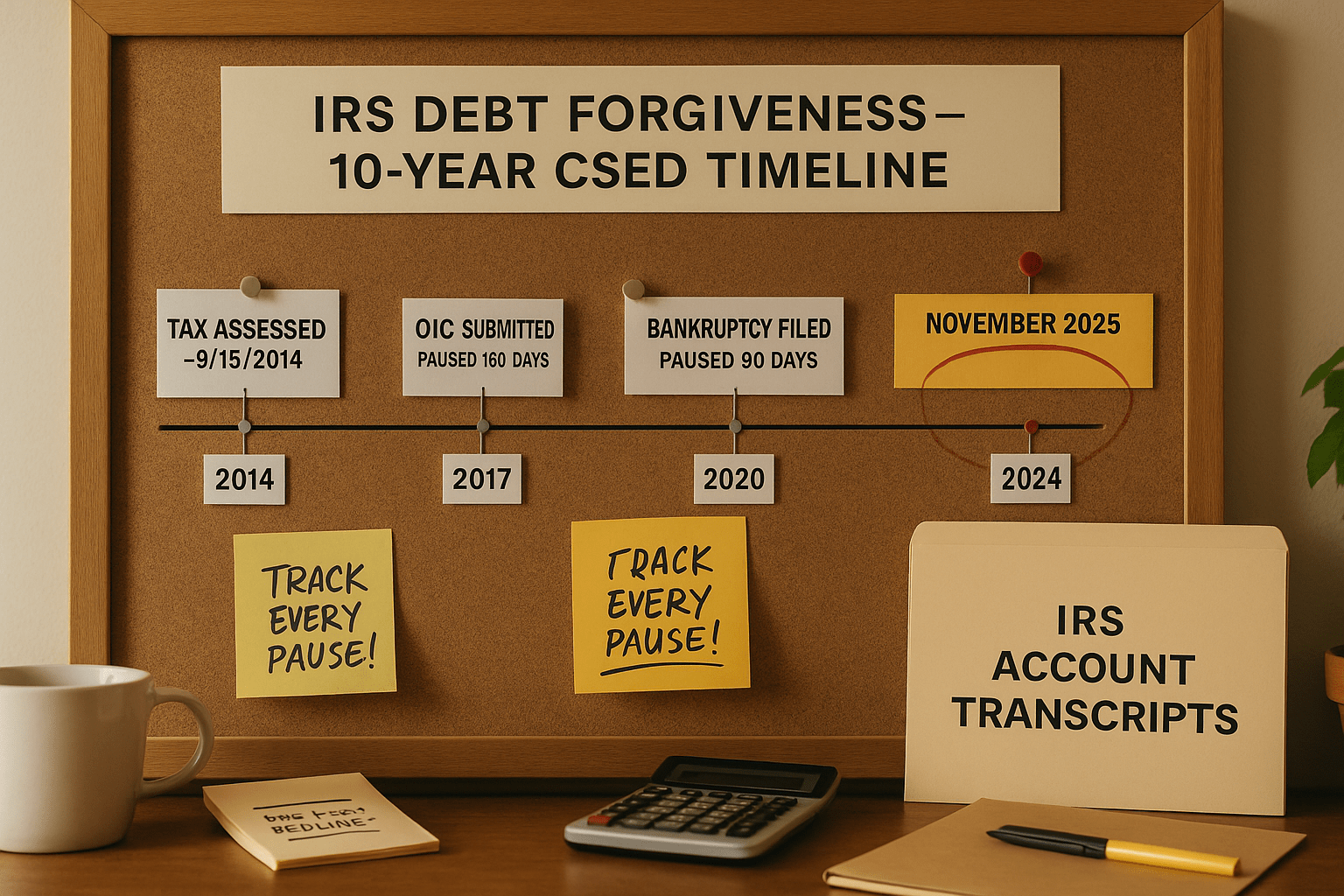

The IRS has exactly 10 years from the date it assesses a tax debt to collect it. This countdown is called the Collection Statute Expiration Date. Once this period ends, the IRS must stop collection activities—including wage garnishments, levies, and liens.

When Does the Clock Start?

The CSED begins when the IRS officially records your tax liability. This is usually the date you file a return or when the IRS makes an assessment through an audit or substitute for return.

What Pauses the CSED?

Certain events stop or extend the 10-year countdown:

- Filing for bankruptcy

- Submitting an Offer in Compromise

- Requesting a Collection Due Process hearing

- Living outside the U.S. for 6 months or more

These pauses can extend the timeline well beyond 10 years if not tracked carefully.

Who Qualifies for IRS Debt Forgiveness After 10 Years?

While many assume the 10-year limit applies automatically, qualification depends on your specific situation.

You Must Have a Valid Assessment

The 10-year period only applies if your debt has been officially assessed. If the IRS files a substitute return on your behalf and you don’t respond, you could miss out on the clock even starting.

Avoid Actions That Restart or Pause the Clock

Even actions like applying for a payment plan or submitting appeals can delay the expiration date. It’s important to track every interaction with the IRS closely.

No New Liabilities

Taxpayers with repeated non-compliance or new unpaid taxes could trigger enforcement even if an old debt is expiring.

How the IRS Tries to Collect Before the Deadline

The IRS actively pursues taxpayers before the 10-year limit runs out.

Wage Garnishments and Levies

If you ignore collection notices, the IRS can garnish wages or freeze bank accounts to recover the amount owed.

Federal Tax Liens

Tax liens can be placed on your home, car, or other property, affecting your credit and ability to sell assets.

Pressure to Settle

The IRS may encourage you to enter installment agreements or submit an Offer in Compromise—both of which pause the CSED and buy the IRS more time.

Risks of Waiting for the 10-Year Limit

While the idea of waiting for IRS debt forgiven after 10 years sounds appealing, it carries serious risks.

Penalties and Interest Pile Up

Even if the IRS can’t collect after 10 years, penalties and interest can make the original debt much larger.

Aggressive Collections

As the expiration date nears, the IRS may take more aggressive action to secure payment, especially for large debts. For help responding to notices or enforcement, visit our legal help center.

No Control Over Timeline Extensions

If you unknowingly take actions that pause the clock, your 10-year window could turn into 12 or even 15 years.

Understanding How IRS Debt Forgiven After 10 Years Works

Yes, IRS debt forgiven after 10 years is possible under the IRS’s statute of limitations. But getting there requires knowing exactly when your CSED starts, avoiding pauses to the clock, and not triggering new IRS enforcement. It’s not automatic, and a misstep could reset the timer entirely.

Talk to a Tax Relief Expert About IRS Debt Forgiveness

If you’re not sure when your 10-year deadline begins or whether you’re close to forgiveness, contact us. Our team can evaluate your IRS history, calculate your expiration date, and help protect your rights while you wait for your tax debt to expire.

Frequently Asked Questions

1. Is IRS debt automatically forgiven after 10 years?

No, but the IRS must stop collection after 10 years if no action has paused or extended the deadline.

2. How do I find out my IRS Collection Statute Expiration Date?

You can request your IRS account transcript or work with a tax professional to calculate your CSED.

3. What if I file for bankruptcy during the 10 years?

Bankruptcy pauses the CSED clock. The pause period is the duration of the bankruptcy plus six months.

4. Can the IRS extend the 10-year statute?

Yes. Actions like submitting an Offer in Compromise or filing appeals can pause or extend the deadline.

5. Will my credit improve if the debt expires?

The IRS doesn’t report to credit bureaus, but expiring liens and collections may still improve your financial standing.

Key Takeaways

- IRS debt forgiven after 10 years is possible through the CSED rule.

- The clock starts when the IRS assesses your debt, not when taxes are due.

- Many actions can pause or extend the expiration period.

- Waiting for forgiveness without a plan is risky.

- A tax professional can help you avoid resets and protect your financial future.

Free Tax Case Review

If you are struggling with tax debt or have received a letter from the IRS complete the form below.

Advertising. This site is a marketing service and does not provide legal or tax advice. Submitting information does not create an attorney-client, tax professional-client, or any other advisory relationship. Results are not guaranteed. A list of participating attorneys, tax firms, and tax providers is available here.

IRS Audit

You received an audit notice from the IRS

Tax Debt Relief

You owe the IRS money and are looking for relief options

Wage Garnishment

The IRS is taking part of your wages to pay off your debt

Tax Lien

The IRS put a legal claim on your property

IRS Property Seizure

The IRS is going to take your property to pay down or pay off your tax debt

Penalty Abatement

You want to request to remove or reduce penalties assessed by IRS

Innocent Spouse Relief

Relief from joint tax debt caused by your spouse or former spouse

Tax Debt FAQ

Common facts, questions and answers about tax debt and tax debt reilef

Tax Debt Lawyer

A tax debt lawyer can help you with your tax debt problems

Recent Posts

- IRS Garnishment Notice Timeline: Understanding Each Step Before Wages Are Withheld

- How IRS Wage Garnishment Works and What Taxpayers Should Know

- Federal Wage Garnishment Limits IRS: Understanding Your Paycheck Protections

- IRS Wage Garnishment Process: A Clear Guide for Taxpayers

- IRS Garnishment Percentage Limits: What Taxpayers Need to Know

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- August 2024

- July 2024

- June 2024

- May 2024

- March 2024

- February 2024

- September 2023

- August 2023

- July 2023

- May 2023

- October 2022